Anatomy of a Startup Cap. Table

One of the first steps in forming a startup, even before any documents are drafted or signed, is creating a capitalization or "cap." table illustrating the ownership of the company.

As companies grow and issue more stock to raise capital or compensate employees, their cap. tables can become long and complicated, yet at the formation stage, cap. tables are relatively simple and require just a few key elements to describe the company's ownership structure (which can then be transcribed into dense legalese by the company's lawyers).

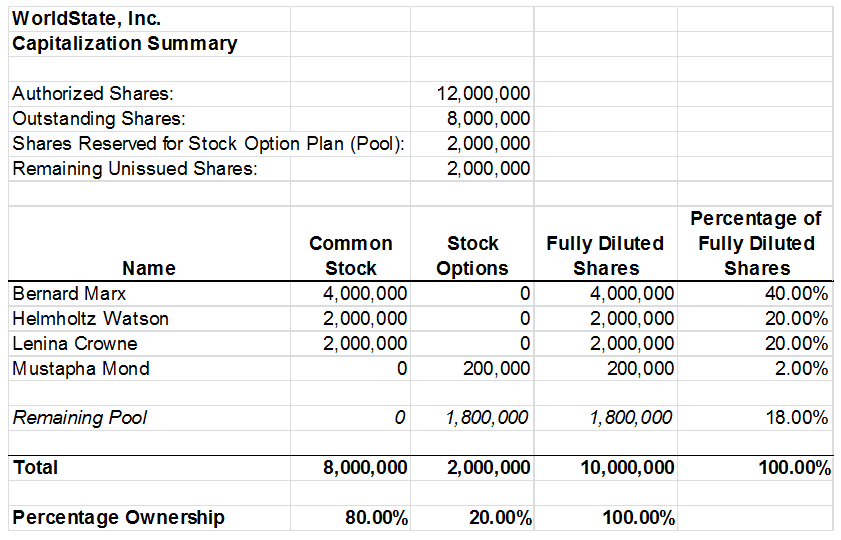

There's no one right way to draft a cap. table, but using a conventional format and common terms make it easier for others to understand. Here is an example of a typical cap. table for a newly formed startup:

Now to explain some of the terms used in the above example:

Authorized Shares: These are all the shares of stock that the company may issue. The number is set in the company's certificate (or articles) of incorporation, the "charter" document that is filed with the state and available to the public, and can only be changed by filing an amendment to the charter. For typical startup companies, this number is in the low seven-figure range, which allows for smaller numbers of whole shares to be granted as options or stock awards to employees or consultants.

Outstanding Shares: These are the shares of stock that have been issued and are still held by the stockholders, which, in the above example, are all the shares of common stock held by the founders or cofounders of the company.

Shares Reserved for Stock Option Plan: These shares are often referred to as the "pool." They are not outstanding shares (no stockholder holds them), but they are reserved or, in other words, set aside, for later issuance by the company when stock options are exercised. Typically, the size of the pool at the formation stage ranges between 10% and 20% percent of the fully diluted shares (explained below). Note that other forms of equity compensation, such as stock awards, may also be granted from this pool, depending on the complexity of the company's equity incentive plan.

Remaining Unissued Shares: These are the leftover authorized shares; shares that are available for the company to issue and that are not otherwise reserved (unlike the shares reserved for the stock option plan). Having a small number of remaining unissued shares can be useful if the company later wants to issue additional stock to a new cofounder or reserve more shares for the pool without filing an amendment to its charter. Note, however, that if the company is a Delaware corporation, it's a good rule of thumb to never have more than half of the company's authorized shares unissued. Otherwise, the company could owe a significantly higher annual franchise tax (see our earlier post on Delaware Franchise Taxes 101).

Fully Diluted Shares: This is the number of shares that would be outstanding if all possible sources of stock were converted or exercised; in the above example, if stock options were granted for all of the shares of stock reserved for the pool and all of those options were fully exercised. Stockholders, especially investors, like to see their ownership expressed in terms of fully diluted shares to conservatively determine the value of their shares, assuming that the entire pool will be used and any options, warrants and convertible notes will be exercised or converted. Note that the percentage of fully diluted shares will typically be lower than the percentages of the "founder split." In the above example, Bernard Marx got 50% of the outstanding common stock, but when Mustapha Mond's option and the remaining pool are factored in, he has only 40% of the fully diluted shares of the company.

For drafting a cap. table for a new startup, that's all the founders should need to know. As the company grows and evolves to higher levels of complexity, so will its cap. table, but the fundamentals of its anatomy explained here will remain the same.

StartupPercolator

StartupPercolator offers access to programs, resources, and dynamic content designed to assist entrepreneurs on their startup journey.